Making Hay While the Sun Shines: Earnings in Focus

Markets eye earnings reports for forward guidance in a challenging environment.

Key Observations

- July provided solid respite after a difficult first half of 2022, with investors buying the dip.

- Investors looked to corporate earnings and guidance to set expectations for the second half of 2022 and beyond, assessing the position of their portfolios while weighing the risk of a recession.

- Analysis showed the primary role of earnings in investment returns over time; earnings have shown a strong, positive trend, a welcome takeaway against a backdrop of negative revisions.

Market Recap

A trying first half of the year for investors saw themes including inflation, geopolitical tensions, tightening conditions and weak corporate guidance dominate headlines. However, fortunes changed in July with the S&P 500 index posting its strongest return since November 2020, up 9.2 percent. An overview of market performance is available in our July 2022 Market Recap. Lying below the reprieve of positive returns were various headlines which invited further speculation and concern. A second consecutive contraction in GDP led to further questions regarding whether we are in a technical recession. June’s Consumer Price Index (CPI) report, released in July, showed a 9.1 percent inflation rate that was both a new multi-decade high and substantially higher than expected. However, growth in personal income and consumption helped fuel a buy-the-dip mentality.

Fixed income markets showed their confidence in the Fed’s ability to combat inflation as medium-term breakevens continued to trend downward – even after a second consecutive 75 bps rate hike by the Fed. Commodity prices rolled over from recent peaks, with WTI crude down to $98.6/barrel as of July 29, 2022 from over $120 earlier this year; industrial metals and agricultural commodities followed suit, yet natural gas prices soared over concerns regarding European gas consumption and their reliance on Russian supply. As earnings season continues, investors have looked for confirmation of analyst estimates and are tuned to management outlooks to set expectations for the second half of the year and beyond. Negative guidance earlier in the year was strongly priced in. Recent, better-than-expected guidance from management has been viewed positively by investors, fueling a buy-the-dip mentality.

Laser Focus on Earnings

Moving into the second half of the year, investors have looked to corporate earnings to glean some information regarding corporate positioning while contending with the risk of a recession. Given the forward-looking nature of markets, prices move more so based on estimates than on numbers reported after the fact, and market prices often lead reported numbers. Earnings reports thus serve as a final check to estimates.

With 56 percent of S&P 500 companies having reported results as of July 29, the blended numbers have been positive but certainly below historical averages. The percentage of S&P 500 companies beating EPS estimates was 73 percent, lower than the five-year average of 77 percent; the average size of the beat was lower as well, at 3.1 percent compared to 8.8 percent over the last five years. Blended earnings growth for the index stands at 6 percent currently, with the blended earnings growth excluding the energy sector at -4.2 percent, the first negative print since the onset of the pandemic in 2020. Energy companies posted exceptional earnings, riding the rally in oil prices over the past year. This contrasts with below-average results for other sectors. Given the pent-up demand and additional stimulus money in consumers’ pockets in 2020 and 2021, record earnings became the norm; thus, year-over-year comparisons would have been difficult in a normal environment with high base effects. Paired with this year’s challenging macroeconomic environment, markets had priced in weak outcomes for the year.

The forward guidance provided by management in their reports serves as the basis for estimates. Part of the drawdown in equity markets earlier this year was driven by prior negative outlooks from management, which highlighted issues like high inflation and interest rates, inventory difficulties, cost pressures, supply chain and staffing issues causing concern. With prices down significantly in the first two quarters, markets had priced in bad news and were prepared for more. However, recent guidance has provided a rosier picture than anticipated, buoying investor’s risk appetites and leading to a strong rally in July.

However, analyst estimates have lagged market realities. While estimates have been revised downward, expectations for the last two quarters and full year 2022 remain rosier than recent outcomes. Estimating company earnings is neither our mandate nor our focus; however, the math tells us companies would need to see a strong recovery in earnings growth in the second half of 2022. Given the current state of the economy, meeting these expectations may prove challenging.

Outlook

While both prices and earnings have trended lower this year, we would caution against trying to call a bottom for either. So far, the bulk of the downward movement has been driven by multiples contracting as the numerator of the P/E ratio, i.e., price, has come down. Attention will shift to the direction of the denominator – markets’ estimates of earnings. If earnings estimates are revised downwards with prices unchanged, the P/E ratio will rise. Thus, additional downward revisions would lead to higher valuations

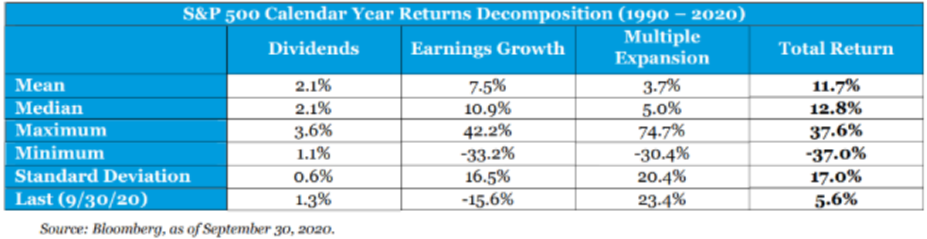

Our research paper, Is Big Tech All You Need?, shows that earnings have demonstrated to be the single largest component of equity returns over time, making up over two-thirds of the S&P 500’s returns from 1990-2020. While volatile, the long-term trend in earnings is strongly positive. Against the backdrop of market volatility and revisions, we outlined our forward-looking assumptions for capital markets in our recent webcast, Mid-Year Capital Markets and Economic Update. Keeping an eye on investing for the long-term and avoiding the risks of market timing, we would drive home the power of earnings compounded over time and maintaining a strategic, disciplined approach to investing.